|

|

|

Промышленный лизинг

Методички

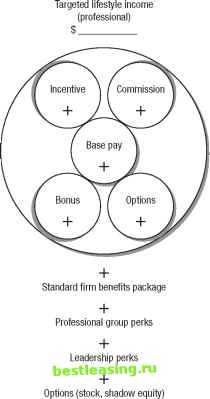

can be found in the Annual Statements Study, published periodically by banking industry trade group Robert Morris Associates.3 Compensation Compensation is not only about money. In a professional services firm, where the most valued assets of the business walk out the door every day, its also about recognition and stability. The elements of compensation create a balance that affords the professional and his or her support staff the peace of mind to focus on the creative work of the firm, thereby enhancing performance (see Exhibit 3.2). Because there are typically few hard assets, sufficient cash flow is critical in maintaining organizational dynamics. In firms where cash flow is a problem, productivity is adversely impacted almost immediately.  Exhibit 3.2 Typical Compensation Options for Professional Services Firms Firms should focus on a targeted lifestyle income range for all employees. This comprehensive look at compensation permits great flexibility in the allocation of benefits (typical cafeteria plans) and in the development of risk management initiatives, such as self-insurance, that the firm may wish to pursue. Firms should also be aware that ongoing, uncritical offers of benefits could turn those benefits from a competitive tool into a potential liability. The subject of compensation, benefits, and staff retention are covered in detail in Chapters 9 and 10. When a Benefit Becomes an Obligation All compensation issues should be reviewed on a regular basis and modified periodically to prevent the potential risk of a benefit turning into a condition of employment. Conditions of employment have been the grist of many court cases and can be construed to occur when companies award the same benefits consistently, and without review or alteration, for many years. When, in hard times, a company suddenly begins to cut back on such benefits, and employees have sued, the courts have often supported the employees claim that the benefit had become a condition of employment. Compensation, or pay for performance, is typically composed of: 1. Base salary 2. Bonus 3. Incentive plan and gain sharing programs (Items that can be subjected to leverage) 4. Options 5. Commissions 6. Employee benefits a. Health, wellness, and lifestyle benefits b. Long-term benefits 7. Professional group perks 8. Leadership perks Regardless of what elements are included in the compensation package, it is important to identify a targeted income level for each principal and employee. Base pay, depending on the nature of the professionals work (e.g., business development versus staff auditing) and the amount of, and leverage potential for, incentive pay usually ranges from 40 percent to 80 percent of total compensation and should be based on comparative wages within the firms geographic region or industry. Numerous sources for comparative salaries exist, including the U.S. Department of Labors Bureau of Labor Statistics,4 various online sources,5 and local development agencies6 that track wages as part of their services in attracting companies to a locality. These sources can also provide extensive lifestyle cost information, including prevailing information concerning employee benefits programs. Bonuses for senior level and other professionals and staff may be established by employment contract, by firm history, or by industry practice. Bonuses are usually discretionary and should be used only to reward extraordinary performance that has been identified and documented. Bonuses are typically paid from profits and represent a share of excess profits before taxes (if a C-Corp), shareholder dividends, reinvestment objectives, and any extraordinary reserves have been paid. Incentive plans and gain-sharing programs are targeted programs designed to promote a limited objective or to spur short-term objectives. These programs will lose some of their potency if they become de facto awards. These plans are often funded as a percentage of gross income for specific lines of business, accounts, or overall revenue gains. Risk/reward calculations (or leverage) are key to developing and administering effective incentive and gain-sharing programs. Options represent rewards given to promising professionals within the firm whom firm principals view as next generation leaders. Options usually offer equity participation at a fixed price to eligible participants. Participants can exercise their options with their own monies or, in some instances, can be underwritten by the firm as a form of sweat equity. The value of options floats with the fortunes of the firm, and participants should receive continuing updates on the value of the firm and their options. Shares associated with options programs are usually restricted and may have additional antidumping provisions. Commissions are normally available only to firm members involved in corporate development and/or sales, although many firms have a finders fee program that extends to all employees who refer new business to the firm. Commission plans proliferate, and plan terms vary by industry and by locality. Principals should consider a few things in establishing any commission program: Commissions should almost never be paid on gross billings (structure them on net income numbers), and commissions should be keyed to net collected revenues. While employees, including principals, want to be paid commissions in a timely manner, either reserving a portion of the commission or delaying the commission until funds are received is recommended. Charge-backs should never be handled as lump sum transactions. If it is necessary to charge back a commission, do it over a period of time. Employee benefits programs usually have two parts: short-term benefits characterized as health, wellness, and lifestyle benefits; and long-term benefits characterized as sustenance benefits. The short-term benefits include health insurance; vacation, sick, and personal days; short-term disability; 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 [ 28 ] 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 116 117 118 119 120 121 122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 148 149 150 151 152 153 154 155 156 157 158 159 160 161 162 163 164 165 166 167 168 169 170 171 172 173 174 175 176 177 178 179 180 181 182 183 184 185 186 187 |