|

|

|

Промышленный лизинг

Методички

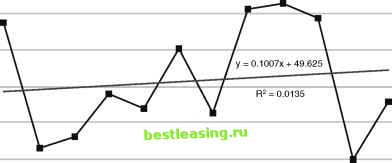

1 2345678 9 10 11 12 Figure 17.15 The slope of the line of best fit provides a good measure of changes over time. This example shows a very typical use for calculating the slope-finding the slope over the previous years usage or billing patterns. The tabular format shows the calculation in a way most suitable for a spreadsheet. However, many data mining tools provide a function to calculate beta values directly from a set of variables in a single row. When such a function is not available, it is possible to express it using more basic arithmetic functions. Although monthly data is often the most convenient for such calculations, remember that different months have different numbers of days. This issue is particularly significant for businesses that have strong weekly cycles. Some months have five full weekends, for instance, while others only have four. Different months have between 20 and 23 working days (not including holidays). These differences can account for up to 25 percent of the difference between months. When working with data that has such cycles, it is a good idea to calculate the average per weekend or average per working day to see how the chosen measure is changing over time. TIP When working with data that has weekly cycles but must be reported by month, consider variables such as average per weekend day or average per work day so that comparisons between months are more meaningful. Revolvers, Transactors, and Convenience Users: Defining Customer Behavior Often, business people can characterize different groups of customers based on their behavior over time. However, translating an informal business description into a form useful for data mining is challenging. Faced with such a challenge, the best response is to determine measures of customer behavior that match the business understanding. This example is about a credit card group at a major retail bank, which has found that profitable customers come in three flavors: Revolvers are customers who maintain large balances on their credit cards. These are highly profitable customers because every month they pay interest on large balances. Transactors are customers who have high balances every month, but pay them off. These customers do not pay interest, but the processing fee charged on each transaction is an important source of revenue. One component of the transaction fee is based on a percentage of the transaction value. Convenience users are customers who periodically charge large amounts, for vacations or large purchases, for example, and then pay them off over several months. Although not as profitable as revolvers, they are lower risk, while still paying significant amounts of interest. The marketing group believes that these three types of customers are motivated by different needs. So, understanding future customer behavior would allow future marketing campaigns to send the most appropriate message to each customer segment. The group would like to predict customer behavior 6 months in the future. The interesting part of this example is not the prediction, but the definition of the segments. The training set needs examples where customers are already classified into the three groups. Obtaining this classification proves to be a challenge. Data The data available for this project consisted of 18 months of billing data, including: Credit limit Interest rate New charges made during each month Minimum payment Amount paid Total balance in each month Amount paid in interest and related charges each month The rules for these credit cards are typical. When a customer has paid off the balance, there is no interest on new charges (for 1 month). However, when there is an outstanding balance, then interest is charged on both the balance and on new charges. What does this data tell us about customers? Segmenting by Estimating Revenue Estimated revenue is a good way of understanding the value of customers. (By itself, this value does not provide much insight into customer behavior, so it is not very useful for messaging.) Basing customer value on revenue alone assumes that the costs for all customers are the same. This is not true, but it is a useful approximation, since a full profitability model is quite complicated, difficult to develop, and beyond the scope of this example. Table 17.5 illustrates 1 month of billing for six customers. The last column is the estimated revenue, which has two components. The first is the amount of interest paid. The second is the transaction fee on new transactions, which is estimated to be 1 percent of the new transaction volume for this example. 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 116 117 118 119 120 121 122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 148 149 150 151 152 153 154 155 156 157 158 159 160 161 162 163 164 165 166 167 168 169 170 171 172 173 174 175 176 177 178 179 180 181 182 183 184 185 186 187 188 189 190 191 192 193 194 195 196 197 198 199 200 [ 201 ] 202 203 204 205 206 207 208 209 210 211 212 213 214 215 216 217 218 219 220 221 222 |