|

|

|

Промышленный лизинг

Методички

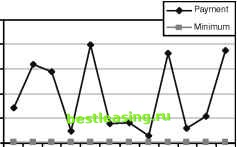

There is another aspect of comparing actual revenue to potential revenue; it normalizes the data. Without this normalization, wealthier customers appear to have the most potential, although this potential is not fully utilized. So, the customer with a $10,000 credit line is far from meeting his or her potential. In fact, it is Customer 1, with the smallest credit line, who comes closest to achieving his or her potential value. Such a definition of value eliminates the wealth effect, which may or may not be appropriate for a particular purpose. Customer Behavior by Comparison to Ideals Since estimating revenue and potential does not differentiate among types of customer behavior, lets go back and look at the definitions in more detail. First, what is it inside the data that tells us who is a revolver? Here are some definitions of a revolver: Someone who pays interest every month Someone who pays more than a certain amount of interest every month (say, more than $10) Someone who pays more than a certain amount of interest, almost every month (say, more than $10 in 80 percent of the months) All of these have an ad hoc quality (and the marketing group had historically made up definitions similar to these on the fly). What about someone who pays very little interest, but does pay interest every month? Why $10? Why 80 percent of the months? These definitions are all arbitrary, often the result of one persons best guess at a definition at a particular time. From the customer perspective, what is a revolver? It is someone who only makes the minimum payment every month. So far, so good. For comparing customers, this definition is a bit tricky because the minimum payments change from month to month and from customer to customer. Figure 17.16 shows the actual and minimum payments made by three customers, all of whom have a credit line of $2,000. The revolver makes payments that are very close to the minimum payment each month. The transactor makes payments closer to the credit line, but these monthly charges vary more widely, depending on the amount charged during the month. The convenience user is somewhere in between. Qualitatively, the shapes of the curves provide insight into customer behavior. $2,000 $1,500 $1,000 $500 $0 $2,500 $2,000 $1,500 $1,000 $500 ф Payment -- Minimum  A typical revolver only pays on or near the minimum balance every month. This revolver has maintained an average balance of $1,070, with new charges of about $200 dollars. A typical transactor pays off the bill every month. The payment is typically much larger than the minimum payment, except in months with few charges. This transactor has an average balance of $1,196. $2,000 $1,500 $1,000 $500 $0 Payment Minimum A typical convenience user uses the card when necessary and pays off the balance over several months. This convenience user has an average balance of $524. Figure 17.16 These three charts show actual and minimum payments for three credit card customers with a credit line of $2,000. Manually looking at shapes is an inefficient way to categorize the behavior of several million customers. Shape is a vague, qualitative notion. What is needed is a score. One way to create a score is by looking at the area between the minimum payment curve and the actual payment curve. For our purposes, the area is the sum of the differences between the payment and the minimum. For the revolver, this sum is $112; for the convenience user, $559.10; and for the transactor, a whopping $13,178.90. This score makes intuitive sense. The lower it is, the more the customer looks like a revolver. However, the score does not work for comparing two cardholders with different credit lines. Consider an extreme case. If a cardholder has a credit line of $100 and was a perfect transactor, then the score would be no more than $1,200. And yet an imperfect revolver with a credit line of $2,000 has a much larger score. The solution is to normalize the value by dividing each months difference by the total credit line. Now, the three scores are 0.0047, 0.023, and 0.55, respectively. When the normalized score is close to 0, the cardholder is close to being a perfect revolver. When it is close to 1, the cardholder is close to being a perfect transactor. Numbers in between represent convenience users. This provides a revolver-transactor score for each customer, with convenience users falling in the middle. This score for customer behavior has some interesting properties. Someone who never uses their card would have a minimum payment of 0 and an actual payment of 0. These people look like revolvers. That might not be a good thing. One way to resolve this would be to include the estimated revenue potential with the behavior score, in effect, describing the behavior using two numbers. Another problem with this score is that as the credit line increases, a customer looks more and more like a revolver, unless the customer charges more. To get around this, the ratios could instead be the monthly balance to the credit line. When nothing is owed and nothing paid, then everything has a value of 0. Figure 17.17 shows a variation on this. This score uses the ratio of the amount paid to the minimum payment. It has some nice features. Perfect revolvers now have a score of 1, because their payment is equal to the minimum payment. Someone who does not use the card has a score of 0. Transactors and convenience users both have scores higher than 1, but it is hard to differentiate between them. This section has shown several different ways of measuring the behavior of a customer. All of these are based on the important variables relevant to the customer and measurements taken over several months. Different measures are more valuable for identifying various aspects of behavior. The Ideal Convenience User The measures in the previous section focused on the extremes of customer behavior, as typified by revolvers and transactors. Convenience users were just assumed to be somewhere in the middle. Is there a way to develop a score that is optimized for the ideal convenience user? 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 116 117 118 119 120 121 122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 148 149 150 151 152 153 154 155 156 157 158 159 160 161 162 163 164 165 166 167 168 169 170 171 172 173 174 175 176 177 178 179 180 181 182 183 184 185 186 187 188 189 190 191 192 193 194 195 196 197 198 199 200 201 202 [ 203 ] 204 205 206 207 208 209 210 211 212 213 214 215 216 217 218 219 220 221 222 |