|

|

|

Промышленный лизинг

Методички

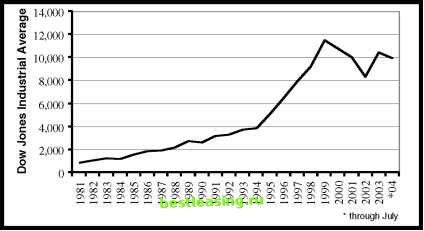

issue suggesting that investors avoid stocks. The cover image was a crashing paper airplane, created from a stock certificate. Stocks were destined to be bad investments, opined the magazine, for the foreseeable future, and the old attitude of buying solid stocks as a cornerstone for ones life savings and retirement has simply disappeared. 12 The pervasive pessimism about stocks in the late 1970s coincided with the best buying opportunity of the century as shown in Figure 3.2. As we see in Figure 3.2, from the end of 1981 until today, the Dow has yielded more than 1,000%, and this calculation does not factor in dividends. As the stock market rose throughout the 1980s and 1990s, the attitudes toward stocks shifted from gloom to glee. Investors gradually increased stock purchases. By the time the stock market peaked in 2000, almost half of U.S. households were invested in mutual funds.13 At the same time, Wall Street firms were advocating 70% investment in stocks, among the highest figures on record.14 The peak enthusiasm for stocks reached in 2000 corresponded with the beginning of one of the worst bear markets since the Great Depression. Sentiment is a predictor of future returns. Optimistic periods tend to be followed by bad performance, whereas pessimism tends to dominate  FIGURE 3.2 The Mother of All Bull Markets Started When Stocks Were Hated Source: Dow Jones before good things happen. Wall Street is driven by greed and fear. The funny thing is that our lizard brains tend to make us greedy when we ought be fearful, and fearful when we ought be greedy. Our ability to be excited at the wrong time extends to individual stocks. Professor Terrance Odean examined the actual trading records of 10,000 ordinary investors.15 He focused part of his study on investors who sold one stock and then bought another stock within a few days. He compared the performance of the stock that was sold with that of the stock that was purchased. How did the investors in this study perform? Remember that if markets were rational, then the stocks that these investors sold would have had the same return (on average) as the stocks that the investors bought. What happened? Professor Odean writes, over a one-year horizon, the average return to a purchased security is 3.3 percent lower than the return to a security sold. So these investors became excited enough to buy and pessimistic enough to sell stocks at the wrong time. Their sentiment was an inverse predictor of success. The efficient markets hypothesis is usually employed to suggest that bargains are impossible. Dont waste your time looking for cheap stocks; if they existed someone else would already have bought them. The converse is also true, but rarely mentioned; if markets were rational, then it would be equally impossible to make systematically bad decisions. Dont waste your time worrying that you might get excited at the wrong time and buy expensive stocks; if they existed someone else would already have sold them. Professor Odean found that markets were mean to these people. The investors studied were completely out of sync with the market. They sold stocks that went up and bought stocks that went down. None of this is supposed to occur if the world ran according to the rules of the efficient markets hypothesis. All stock prices are supposed to be correct, so it should be impossible to make systematically bad choices. In an episode of the futuristic cartoon, The Jetsons, there is a mobile, robotic slot machine that rolls around enticing would-be gamblers by saying, Im due. The implication is that no one has hit the jackpot in a while so now is a good moment to invest a few bucks to try to win. The punch line of the scene comes when some lucky gambler actually does win the jackpot. The robot pays out the money and then scoots off proclaiming, Im due. In reality, slot machines are never due. They are designed to completely forget the past; in the language of probability, slot machines are memoryless. The chance of winning immediately after a jackpot is the same as on a slot machine that has gone years without a winner. The efficient markets hypothesis states that stock markets should be memoryless like an idealized slot machine. Nothing should predict the next days stock price changes. So if it were true that optimism preceded stock (and stock market) declines, then that would be evidence of market irrationality and market meanness. The Denial: The believers in the efficient markets hypothesis deny that sentiment provides any information about future price changes. They claim that the evidence of disdain for stocks in the late 1970s (e.g., the Death of Equities cover story) is anecdotal and thus not scientific. Professor Odeans study demonstrating irrationality must be flawed. Photographic Evidence: Scientific Evidence of Sentiment Predicting Stock Price Changes Professor Richard Thaler, doyen of the behavioral school, and Professor Werner DeBondt performed a systematic analysis of sentiment.16 They hypothesized that people would feel good about rising stocks and feel bad about falling stocks. Therefore, they predicted that the future performance of stocks that made investors feel bad (the losers) would be better than that of stocks that made investors feel good (the winners). Professors Thaler and DeBondt thus predicted that a way to make money is precisely to buy the hated stocks that had been losers. They performed a systematic study of hundreds of stocks over many years. In each period they constructed a portfolio of previous winners and previous losers. They then compared the performance of their winner and loser portfolios. 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 [ 17 ] 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 |