|

|

|

Промышленный лизинг

Методички

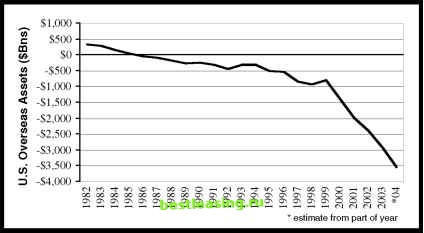

dollar fell from just over 1 U.S. dollar in 1976 to a low of 63 cents and has remained below 75 U.S. cents for almost 10 years. Canadas adjustment process was not painless, but it was relatively gradual and did not involve any panics. In contrast, Mexico took the Kellermans route. In the mid-1980s, my buddies and I used to make surf trips from San Diego down to Mexicos Baja peninsula. Along the way we saw advertisements for Mexican investments guaranteed to return 40% per year. This seemed like an amazing deal, and some of my friends took up the offers. For a time, my surf friends earned high interest rates on their Mexican investments. The process was very simple: Convert some U.S. dollars into Mexican pesos and invest the pesos for a year. Earn 40% on your pesos in a year, get them back, and convert your pesos into dollars. A $1,000 investment returned $1,400 just 12 months later. Not too shabby! Furthermore, the deposits were guaranteed to return 40% more pesos than invested. There are few things more expensive than free lunches, especially in the investing world. The catch is that the Mexican deposits were guaranteed to return 40% more in pesos. The dollar value of those pesos was not guaranteed. Not to worry, though, how much can a peso devalue in a year? As you might expect, this story involves the Mexican current account. In the early 1990s, Mexico was running a current account deficit that was 7% the size of its economy. As we have learned, such deficits are unsustainable and the road to repayment usually includes devaluing the currency. In late 1994, a Mexican peso was worth about 30 U.S. cents. One year later it was worth about 12 cents.8 Now consider the 40% guaranteed return on your peso investment. Your $1,000 still earns 40% in pesos, but when the proceeds are converted back into dollars the investment returns about a total of $500. Rather than earning a 40% positive return, this guaranteed investment lost half its value in one year. While the Mexican peso devaluation was bad for foreign investors, it was a crisis for Mexicans and many others. In simplest terms, the adjustment from current account deficit to surplus requires a change in wealth. Both Canadians and Mexicans became poorer because of their currency devaluations. The speed of the Mexican decline caused panic and severe readjustment costs. The U.S. current account deficits will end. The adjustment path can be rocky or smooth. The U.S. situation is different, and in many ways better, than either the Canadian or the Mexican current account deficits. These differences lead many pundits to confidently predict a smooth path. Because the U.S. current account deficit is the largest in history, however, there is no precedent. Therefore predictions of the adjustment path are simply speculations, some well grounded, but speculations nonetheless. The Country with the Golden Brain Since the United States is in a dominant economic position, perhaps the best predictor of the coming current account adjustment lies neither north nor south of the border, but in our own history. In the early 1980s, the U.S. current account deficit reached then record highs (although Figure 6.1 shows that these deficits pale in comparison to more recent deficits). What happened after record U.S. current account deficits in the early 1980s? Well, the most common effects of large current account deficits are clear in this case. First, the current account deficits shrank. Second, the move away from deficit was accompanied by a substantial weakening of the dollar.9 This 1980s bout of U.S. current account adjustment was very smooth; much more like the Canadian experience than the Mexican peso crisis. Should we then infer that the coming adjustment will also be relatively smooth? Perhaps, but the current situation differs for two reasons. First, the current U.S. deficits are much larger than those in the 1980s. Second, in the last few decades the United States has moved from being the worlds biggest creditor to the biggest debtor. The protagonist in Alphonse Daudets Man with the Golden Brain is born with a skull full of precious metal-his brain is literally made of gold. Throughout his life, he spends his birthright to help his parents and then his beautiful wife. He is particularly lavish with his spouse and spoils her with gifts paid for by depleting his finite supply of metal. For each purchase, he must remove part of his brain and sell the precious supply for cash. When the man with the golden brains wife dies, he spares no expense on the funeral. On his way home from the cemetery, he stops to buy a pair of blue satin boots. The store clerk hears a scream and rushes to find the man clutching the boots in one hand, while the other hand is covered with blood and contains gold scrapings at the ends of the nails. His golden birthright was gone; his entire brain sold off bit by bit over the years. In a far less dramatic manner, but to a far greater degree, over the last several decades the United States has spent its golden treasure. Figure 6.2 depicts how the United States has changed from an international creditor to a debtor. The figures are calculated by adding up all the U.S. investments abroad and then subtracting foreign investments in the United States.  FIGURE 6.2 The United States Is the Biggest Debtor in the World Source: U.S. Commerce Department 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 [ 43 ] 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 |