|

|

|

Промышленный лизинг

Методички

0л= - 1 will cause a downward revision in P. There is only one case in which P and Op are uncorrelated: when the adverse-selection component of the spread is zero. Implications for Transaction Price Dynamics To derive implications for the dynamics of transactions prices, denote by f the revisions in Pn-\ due to the arrival of new public information between traces n-1 and n. Then the nth transaction price maybe written as P = / , +e + /1 Q . Takijig the first difference of (3.2.20) then yields (3.2.25) P -P -\ = (/ -/J -i) + (c G. -C, ,CJ, ,) (3.2.26) = AnQj, + e + {c Qj, - C , (3.2.27) which shows that transaction price changes arc comprised of a gross-profits component which, like Rolls (1984) model of the bid-ask spread, exhibits reversals, and an adverse-selection component that lends to be permanent. Therefore, Glostcns attribution of the effective spread to ihe gross-profits component is not coincidental, but well-motivated by the fact that il is this component that induces negative serial correlation in returns, not the adverse-selection component. Accordingly, Gloslen (1987) provides alternative relations between spreads and return covariances which incorporate this djstmction between the adverse-selection and gross-profits components. In particular, under certain simplifying assumptions Gloslen shows thai2 E[/<*] = IW+yfi), Cov[ ,\ n J = (3.2.28) where P, (Pa + Pb)/2 С + Л </4) ir I and where Л , R, arc the per-period market and true returns, respectively, and ?ц is the continuously compounded per-period market return. These relations show that the presence of adverse selection (y < 1) has an additional impact on means and covariances of returns that is not captured by other models of the bid-ask spread. Whether or not the adverse-selection Specifically, he assumes thai: (1) True returns ait independent of all past history: (-1 fire spread is symmetric about the true price; and (3) the gross-profit component docs not cause conditional drift in prices. component is economically imporlanl is largely an empirical issue that has yet lo be determined decisively,21 nevertheless Glostcns (1987) model shows thai adverse selection can have very different implications for the statistical properties of transactions data than other components ol the bid-ask spread. 3.3 Modeling Transactions Data One of the most exciting recent developments in empirical finance is the availability of low-cost transactions databases: historical prices, quantities, bid-ask quotes and sizes, and associated market conditions, transaction by transaction and time-stamped to the nearest second, for example, the NYSEs Trades and Quotes (TAQ) database contains all equity transactions reported on the Consolidated Tape from 1992 lo the present, which includes all transactions on the NYSE, AMEX, NASDAQ, and the regional exchanges. The Berkeley Options Database provides similar data for options transactions, and transactions databases for many other securities and markets are being developetl as interest in market microstructure issues continues lo grow. The advent of such transactions databases has given financial economists ihe means to address a variety of issues surrounding lite line structure of the trading process or price discovery, for example, what are determinants of the bid-ask spread, and is adverse selection a more important factor than inventory costs in explaining markclmaking behavior?2 Does the very act of trading move prices, and if so, how large is this price impact effect and how does it vary with the size of lite Hade?21 Why do prices tend to fall mote often or. whole-dollar multiples than on half-dollar multiples, more often on half-dollar multiples than on quartet-dollar multiples, etc.?27 What arc the benefits and costs of other aspects of a markets microstructure, such as margin requirements, the degree of competition laced by dealers, the frequency thai orders are cleared, and iulraday volatility?28 Although none of 1 Recent attempts to quantify the relative conuibulionsol order-processing/inventory costs and adverse selection costs to the bid-ask spread include: Allleck-Graves, Hegde, and Miller (1994), Gloslen and Harris (1УЙ8).George. Kaul, and Nimalemlran (1УУ1). Huang and Stoll (1995a), anil Stoll (1У8У). See Section 3.4.2 for further discussion. See Aiuihud and Mendelson (1980), llagehol (1У71). Copeland and Galai (1983), Ucm-sctz (19(38), Kasley and OTlara (1987), Gloslen (1987), Gloslen and Harris (1988), Glostcn and Milgrom (198.1), I lo and Stoll (1981). Stoll (1978, I9H9). and Tinic (1972). -See Ik-iLsimas and I.o (I99(i), Chan and bikonisbok (1993b, 199.1), and Keim and Mad-havan (199.1a,1), 199(1). -See Ball, Torous. and Tschoegl (198.1); Christie. Harris, anil Schullz (1994); Christie and Schultz (1994); Goodharl and Cnrrio (1990); Harris (1991); Niedeiholler (190.1, I9(i(i); Nicdcrhollcr and Osborne (19ti(>); and Osborne (1У02). -*See Cohen, Maier, Schwartz, ami Whitcomb (198(1), I lai lis. Solianos, and Shapiio (1994), llasbrotick (1991a. !>), Madhavan and Smidi (1991), and Stoll and Wbaley (1990). these questions arc new lo llit- rrccnl lilcralurc, ihc kind of answers we can provide have changed dramatically, thanks lo transactions data. Even the event study, which traditionally employs daily returns data, has heen applied recently to transactions data to sill out the impact of news announcements til /)/ the day (see, lor example, Barclay and l.itzenbcrgcr [ 1088]). The richness ol these datasets does not come without a price-transactions dalasels are considerably more difficult to manipulate and analyze because of their sheer si/e. For example, in 1994 the NYSK consummated \) over -1!) million transactions, and for each transaction, the NYSEs Trades J and Quotes (TAQ) database records several pieces of information: transac-i lion price, time of trade, volume, and various condition codes describing i the hade, bid-ask quotes and depths are also recorded. Even for individual securities, a sample size of 100,000 observations for a single year of transactions data is not unusual. j l.l.l Motivation , Transactions data post a number of unique econometric challenges that j do not easily lit into the framework we have developed so far. Tor exam-I plo, transactions data are sampled at irregularly spaced random intervals- j whenever trades occur-and this presents a number of problems for stan- dard econometric models: observations are unlikely to be identically dis-j irihulcd (since some observations are very closely spaced in lime while others I may he separated by hours or days), it is difficult to capture seasonal effects ! (such as time-ol-day regularities) with simple indicator functions, and fore-j casting is no longer a straightforward exercise because the transaction times I are random. Also, transaction prices are always quoted in discrete units or ticks- currently $0. 125 for equities, $0.0025 for equity options, $0.05 for futures contracts on the Standard and Poors 500 index, $0.03125 for US Treasury bonds and notes, and so on. While there are no a priori theoretical reasons to rule out continuous prices, the transactions costs associated with quoting and processing such prices make them highly impractical.- Of course, -Despite ilie indivisibilities ili.ii ai i onip.iuv pi ire discreteness, there seems iii be gcnri.il agreement .iiiiimg c< ouoinisis ami pt.irtiliouris alike dial die cllicicncv gains Itum disi ictr piiccs lai outweigh dir poii-nlial costs til indivisible trading lots. 1 lowrvcr. an unresolved issue is tbe afttntiitl iti-gitr nl disc leleness, which balances the costs оГ indivisibilities against lite beuelils ol discreteness, for example, on the NYSK, tile nnuimmn price movement of slocks with prices grcairi than or eipral lo $1 is one lick, bin this minimum price variation was set yean, ago hcloic the advent ol high-speed digital computers and corresponding electronic trading mei luuisms. It is nut leal whether 01 not an eighth ol a dollar is die optimal degree ol ilisi teletiess today. Indeed, iiienl disi ussions between the NYSK and the US Sri unties and l-.xch.uigc (lomiiiissioii serin lo indicate a tuovr towards ilniimttiznlnni under which pi ices and (limits are denominated m cents. See Hall, Tomus. and Tschocgl (lWr>); Ivu-nnan and < jiprland (I.IKX); Man is (I.KI It:.untitle SI Csllllilll Mmkrl 2l)(Kt\\udv tin liinhei discussion.

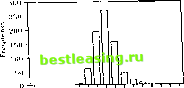

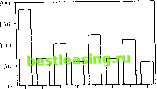

Summary slaiisiics for daily returns data from January 2,1990, to December 31,1992, for five NYSK stocks: AAC = Anacoinp; APD = Air Products and Chemicals; CBS = Columbia Uroadcasling System; CCB = Capital Cities ARC; KAB = Kaneb Services. / , 5.250 / 1.375 T> 3.353 At I) 0.811 discreteness is less problematic for coarser-sampled data, which may be well-approximated by a continuous-state process. But it becomes more relevant for transaction price changes, since such finely sampled price changes typically take on only a few distinct values. For example, the NYSE Fact Book: 1V94 Data reports that in 1994, 97.4% of all transactions on the NYSE occurred with no change or a one-tick price change. Moreover, price changes greater than 4 ticks are extremely rare, as documented in Hausman, lx>, and MacKinlay (1992). Discreteness and Prices Discreteness affects both prices and returns, but in somewhat different Ways. With respect to prices, several studies have documented the phenomenon of price clustering, the tendency for prices to fall more frequently on certain values than on others.* For example, Figure 3.2a displays the histograms of the fractional part of the daily closing prices of the following five NYSE slocks during the three-year period from January 2, 1990, to December 31, 1992 (see Table 3.1 for summary statistics): Anacomp (AAC), Air Products and Chemicals (APD), Columbia Broadcasting System (CBS), Capital Cities See. (or example. Ball, Torous, and Tschoegt (1985); Coodhart and Curcio (1990); Harris (1941): Niiderholler {1 . ( >. .. Hlliti); Niederholler and Osborne (19()6); and Osborne (19(12). Table 3.1. Summary statistics for daily returns offive NYSE stocks iiwuto AAC AFP CBS CCB KAB 86.750 216.500 629.750 7.250 40.625 129.000 360.250 2.875 55.878 173.924 467.844 4.665 11.380 18.877 53.251 0.816 AlfC (CCB), and Kancb Services (КЛВ). The histogram Cor CBS is a particularly good illustration of the classic price-clustering pattern: Prices tend tojfall more frequently on whole-dollar multiples than on half-dollar inul-lip les, more frequently on half-dollars than on quarter-dollars, and more frequently on even eighths than on odd eighths. Price-clustering is even more pronounced for transactions data. The importance of these patterns of discreteness has been highlighted 3£ by the recent controversy and litigation surrounding the publication of two empirical studies by Christie and Schultz (1994) and Christie, Harris, Ж and Schultz (1994). They argue that the tendency for bid-ask quotes on ft*- N/iSDAQ slocks to cluster more frequently on even eighths than on odd сц hlhs is an indication of tacit collusion among NASDAQ dealers lo main- w tai ir wider spreads. Of course, there are important differences between the У NASDAQs market structure and those of other organized exchanges, and more detailed analysis is required to determine if such differences can ex-1ЩР phiin the empirical regularities documented by Christie and Schultz (1994) antl Christie, Harris, and Schultz (1994). Although the outcome of this controversy is yet to be decided, all parties concerned would agree that discreteness can have a tremendous impact on securities markets. Discreteness and lhlurns The empirical relevance of discreteness/or returns depends to a large extent on the holding period and the price level, for reasons that wc shall discuss below. For transactions data, discreteness is considerably more problematic because the price change from one transaction lo the next is typically only one or two licks. For example, if the minimum price variation is an eighth of a dollar, a stock currently priced at $10 a share can never yield a transaction return between zero and ±1.25%. In fact, in this case, the transaction return must fall on a discrete grid of integer multiples of 1.25%. For higher-priced stocks, this grid is considerably finer. For example, the transactions return for a $50 stock will fall on a grid of integer multiples of 0.25%. Moreover, as the price level varies through lime, die collection of transaction returns obtained may seem less discrete because the grid corresponding lo the entire datasel will be the superposition of die grids al each price level. Therefore, if price levels are high and volatile, or if the tiinespau of the datasel is long (which implies higher price-variability under a random walk model for prices), the discreteness of transaction returns will be less apparent. Table 3.2 contains a concrete example of this intuition. It reports the relative frequencies of transaction price changes for the five stocks in Fig- M Other4 contributions to the NASDAQ controversy include Chan, Christie, and Schultz (199Г0, Furbish and Smith (НПС)), Godek (WKi), Grossman. Miller, Fischel, Came, and Koss (1УЛ15), Huang and Stoll (1.1.1Г>1>). Kandel and Marx (Hl.lti). and Kleidon and Willig (II.lj). so -mi -Hi -in 1  II . 12f> .2MI .:17Г, .Г.1Н1 .li2.r> .7MI .Н7Г 1iui tt; n. (<u ЛЛС. -i-i-I-r . - - -к -ii -i -ч ii i * t, к Iliie Change ll k>) 1 Г ЛЛО 1T.0 lai <m -mi -:iii -

ti - т т -г т 0 .1 -jr. .2Г>П ..ч7г1 ,Г>(Н1 .<>2Г. .7г1<1 .н7г 1-й I ,. (!..и ttu Л1М) I -2 II a 4 <i к Ill, с- < Ьлпц. (и. Ы l i Л1Ч)  :uiii 2Г>1> - = 204-I. 5- ir.o * 1(111- II I.Ti .ZWI .Л7Г> .Mill .IKS .7!i(l H7 i- Fi; iii>n loi CHS  О .12Г> .2Г>1) .:17Г. .ГНШ .liZri ,7Г>(1 .Н7Г< Pine Kiarlion 1ш CCIt . , . i V i 7 rV i t tlt T И -li -I -2 II 2 4 l> И ГГ., i-CI.....BHl W lot ecu I.II KIN C KU z 1,11 i -hi 211 -  II 2Г> 2Г .Л7Г> .Mill .1>2Г. .7MI .Н7Г Il i< г Fi.u поп tor КЛН -Я -II -I -2 II 2 I 4 К Pint- С1.мцс- (lii k-.) lur КЛВ (l>) Figure 3.2. Histogram of Daily Price Fractions and Price OumgesforFhv NYSE Stocks ft January!, 1990 lo December 31, 1992 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 [ 19 ] 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 |