|

|

|

Промышленный лизинг

Методички

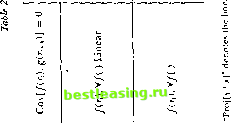

2. The/ит. lability (ij Asset Returns (he notion of long-range dependence, and a test for litis phenomenon is presented in Section 2.1). For completeness, we provide a brief discussion of tests for unit roots, which are sometimes confused with tests of the random walk. In Section 2.8 we present several empirical illustrations that document important departures from the random walk hypothesis for recent US stock market data. 2.1 The Random Walk Hypotheses Л useful way to organize the various versions of the random walk and martingale models that we shall present below is to consider the various kinds of dependence that can exist between an assets returns r, and r,+* at two dates / and I + k. To do this, define the random variables /(/>) and g{r,+k) where /( ) and g(-) are two arbitrary functions, and consider the situations in which ( ovi/o-a.guvoH = о (2.1.D for all / and for AtO. For appropriately chosen /( ) and g(), virtually all versions of the random walk and martingale hypotheses are captured by (2.1.1), which may be interpreted as an orthogonality condition. For example, if /( ) and g{-) are restricted lo be arbitrary linear fur.c-tions, then (2.1.1) implies that returns arc serially uncorrected, corresponding to the Random Walk 3 model described in Section 2.1.3 below. Alternatively, if /( ) is unrestricted but g(-) is restricted to be linear, then (2.1.1) is equivalent to the martingale hypothesis described in Section 2.1. Finally, if (2.1.1) holds for all functions /( ) and g(-), this implies that returns are mutually independent, corresponding to the Random Walk I and Random Walk 2 models discussed in Sections 2.1.1 and 2.1.2, respectively. This classification is summarized in Table 2.1. Although there are several other ways to characterize the various random walk and martingale models, condition (2.1.1) and Table 2.1 are particularly relevant for economic hypotheses since almost all equilibrium asset-pricing models can be reduced to a set of orthogonality conditions. This interpretation is explored extensively in Chapters 8 and 12. The Martingale Model Perhaps the earliest model of financial asset prices was the martingale model, whose origin lies in die history of games of chance and the birth of prol>-ability theory. The prominent Italian mathematician C.trolatno Cardano proposed an elementary theory of gambling in his 151)5 manuscript Liber de  Ludo Aleae (The Book of Games of Chance), in which he wrote:1 The most fundamental principle of all in gambling is simply equal run-dilions, e.g., of opponents, of bystanders, of money, of situation, >i die dice box, and of the die itself. To the extent lo which you depail lioin thai equality, if it is in your opponents favour, you are a fool, and if in your own, you are unjust. This passage clearly contains the notion of a fair game, a game which is neither in your favor nor your opponents, and this is the essence of a martingale, a stochastic process /,} which satisfies the following condition: K[/1+1 I P /,- ...] = P . (2.1.2) or, equivalently, KUh-i - Ii ! I Л-ь... 1 = 0. (2.1.3) If P, represents ones cumulative winnings or wealth at date I from playing some game of chance each period, then a fair game is one for which the exp-cted wealth next period is simply equal to this periods wealth (see (2.1j.2)), conditioned on the history of the game. Alternatively, a game is fair if lite expected incremental winnings at any stage is /.его when conditioned on the history of the game (see (2.1.3)). If Pt is taken to be an assets price at date t, then the martingale hypothesis states that tomorrows price is expected to be equal to todays price, given the assets entire price history. Alternatively, the assets expected price charige is zero when conditioned on the assets price history; hence its price is jut as likely to rise as it is to fall. From a forecasting perspective, the martingale hypothesis implies that the best forecast of tomorrows price is simplly todays price, where best means minimal mean-squared error (see Chapter 7). Another aspect of the martingale hypothesis is that nonoverlapping price changes arc uncorrected at all leads and lags, which implies the in-effec ;iveness of all linear forecasting rules for future price changes based on historical prices alone. The fact that so sweeping an implication could comcj from as simple a model as (2.1.2) foreshadows the important role that the martingale hypothesis will play in the modeling of asset price dynamics (see the discussion below and Chapter 7). In fact, the martingale was long considered to be a necessary condition lor an efficient asset market, one in which the information contained in past prices is instantly, fully, and perpetually reflected in the assets current price. If the market is efficient, then it should not be possible to profit by trading on See llald (1990, Chapter 4) fur further details. 2See Samuelson (1965, 1972. 19711). Roberts (1%7) calls the tnaninjrale hypothesis uvuk-form market efficiency. Me also detiues an asset m.ukel lo be \rmistmng-fnnn and \/нше шш the information contained in the assets price history; hence the conditional expectation of future price changes, conditional on the price history, cannot be either positive or negative (if shorlsalcs are feasible) and therefore must be zero. This notion of efficiency has a wonderfully counterintuitive and seemingly contradictory flavor to it: The more efficient the market, the more random is the sequence of price changes generated by the market, and the most efficient market of all is one in which price changes are completely random and unpredictable. However, one of the central tenets of modern financial economics is die necessity of some trade-off between risk and expected return, and although the martingale hypothesis places a restriction on expected returns, it does noi account for risk in any way. ln particular, if an assets expected price change is positive, it may be the reward necessary to attract investors to hold the asset and bear its associated risks. Therefore, despite the intuitive appeal that the fair-game interpretation might have, it has been shown that the martingale property is neither a necessary nor a sufficient condition for rationally determined asset prices (see, for example, I.eroy [1973], Lucas [1978], and Chapter 8). Nevertheless, the martingale has become a powerful tool in probability and statistics and also has important applications in modern theories of asset prices. For example, once assel returns are properly adjusted lor risk, the martingale property does hold (see Lucas [ 1978], Cox and Ross [ 1976], Harrison and Krcps [1979]). In particular, we shall see in Chapter 8 that matginal-uulity-weighled prices do follow martingales under quite general conditions. This risk-adjusted martingale property has led to a veritable revolution in the pricing of complex financial instruments such as options, swaps, and other derivative securities (see Chapters 9, 12, and Merlon [1990], for example). Moreover, the martingale led to the development of a closely related model that has now become an integral part of virtually every scientific discipline concerned with dynamics: the random walk hypothesis. 2.1.1 The Random Walk 1: IID Increments Perhaps the simplest version of die random walk hypothesis is the independently and identically distributed (IID) increments case in which the dynamics of (/,) are given by the following equation: P, = м + +e (, ~ IID(0,o-2) (2.1.4) where ji is the expected price change or drift, and 110(0, a2) denotes thai e, is independently and identically distributed with mean 0 andai iance cr. The elhcient if the conditional expectation of future price changes is /его. conditioned on all available public information, and all available public and private information, respectively. See Chapter 1 lor further discttvsioll оПЬсчс cojk epts. independence of die increments jf,) implies thai die random walk is also a fair game, hut in a much stronger sense than the martingale: Independence implies not only that increments are nncorrelated, hut that any nonlinear functions of the increments arc also uncoirelated. We shall call this the Random Walk I model or RWl. To develop some intuition for RWl, consider its conditional mean and variance at date /, conditional on some initial value /> at dale 0: Ki/, I / I = l\, + nt (2.1.5) Var/, I / = aI, (2.1.C.) which follows from recursive substitution of lagged P, in (2.1.4) and the 111) increments assumption. From (2.1.5) and (2.1.6) it is apparent that the random walk is nonstationary and that its conditional mean and variance are both linear in lime. These implications also hold for the two other forms of the random walk hypothesis (RW2 and RW3) described below. Perhaps the most common distributional assumption for the innovations or increments t, is normality. If the e/s are IID JV(0, a-), then (2.1.4) is equivalent to an arithmetic linmminn motion, sampled at regularly spaced unit intervals (see Section 9.1 in Chapter 9). This distributional assumption simplifies many of the calculations surrounding the random walk, but suffers front the same problem that afflicts normally distributed returns; violation of limited liability. II (he conditional distribution of/ is normal, then there will always be a positive probability that / <0. To avoid violating limited liability, we may use the same device as in Section 1.4.2, namely, to assert that the natural logarithm of prices p, = log/, follows a random walk with normally distributed increments; hence / = +/., , +e e, 1ЮЛГ(0,а-). (2.1.7) This implies that continuously compounded returns are IID normal variatcs with mean /1 and variance a-, which yields the lognormal model of Bachelier (1900) and F.iustein (1905). We shall return to this in Section 9.1 of Chapter 9. 2.1.2 The Random Walk 2: Independent Increments Despite the elegance and simplicity of RWl, the assumption of identically distributed increments is not plausible for financial asset prices over long lime spans. For example, over the two-hundred-ycar history of the New York Slock Exchange, there have been countless changes in the economic, social, technological, institutional, and regulatory environment in which stock prices arc determined. The assertion thai the probability law of daily stock returns has remained the same over this two-hundred-year period is simplv implausible. Therefore, we relax the assumptions of RWl to include processes with independent but not identically distributed (INID) increment, and we shall call this the Random Walk 2 model or RW2. RW2 clearly contains RWl as a special case, but also contains considerably more general price prcf cesses. For example, RW2 allows for unconditional heteroskedasticity in the 6(s, a particularly useful feature given the time-variation in volatility of many financial asset return series (see Section 12.2 in Chapter 12). Although RW2 is weaker than RWl (see Table 2.1), it still retains the most interesting economic property of the IID random walk: Any arbitrary transformation of future price increments is unforecastable using any arbitrary transformation of past price increments. 2.1.3 The Random Walk 3: Uncorrelaled Increments Ал even more general version of the random walk hypothesis-the one most often tested in the recent empirical literature-may be obtained by relaxing the independence assumption of RW2 to include processes with dependent but uncorrected increments. This is the weakest form of the random walk hypothesis, which we shall refer to as the Random Walk 3 model or RW3, and contains RWl and RW2 as special cases. A simple example of a process that satisfies the assumptions of RW3 but not of RWl or RW2 is any process for which Cov[e e, ] = 0 for all h ф 0, but where Cov[e, e* t] ф 0 for some кфО. Such a process has uncorrelated increments, but is clearly not independent since its squared increments are correlated (see Section 12.2 in Chapter 12 for specific examples). 2.2 Tests of Random Walk 1: IID Increments Despite the fact that RWl is implausible from a priori theoretical considerations, nevertheless tests of RWl provide a great deal of intuition about the behavior of the random walk. For example, we shall see in Section 2.2.2 that the drift of a random walk can sometimes be misinterpreted as predictability if not properly accounted for. Before turning to those issues, we begin with a brief review of traditional statistical tests for the IID assumptions in Section 2.2.1. 2.2.1 Traditional Statistical Tests Since the assumptions of IID are so central to classical statistical inference, it should come as no surprise that tests for these two assumptions have a long and illustrious history in statistics, with considerably broader applications than to the random walk. Because of theirbreadth and ubiquity, it is virtually 1 2 3 4 5 [ 6 ] 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 |