|

|

|

Промышленный лизинг

Методички

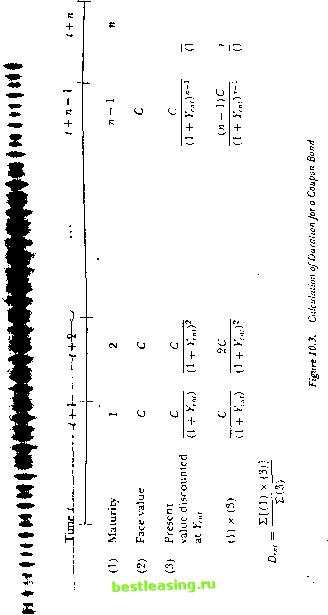

i iii iii ihiii .111 ii lillls nine / t + n Hity I (и + 1 )->crioil -/ ., i , bond Sell/> + [)p, r +L (-period bonds Im I P, Net 0 Figure 10.2. C.nsli flaws in a Fontvird Transaction Moving to logs Cor simplicity, die n-pcriod-ahcad log forward rale is jni = Im - 1>нл\.1 = ( + I) V,h-1.i - y < = \>и l.i + (> -1, i ~ y i) = >/ + ( + 1 )(vM+i. t-y t). (10.1.8) Equation (10.1.8) shows that the forward rate is positive whenever discount bond prices fall with maturity. Also, the forward rale is above both the n-period and the (n + l)-period discount bond yields when the (n + l)-period yield is above the н-period yield, that is, when the yield curve is upward-sloping.7 This relation between a yield lo maturity and the instantaneous lorward rale at thai maiuriiy is analogous lo the relation between marginal and average cost. The yield lo maturity is the average cost of borrowing for i periods, while the forward rale is the marginal cost of extending the time period of the loan. Figure 10.1 illustrates the relation between the forward-rate curve (shown as a dashed line) and the yield curve (a solid line). The forward-rate curve lies above the yield curve when die yield curve is upward-sloping, and below it when the yield curve is downward-sloping. The two curves cross when the yield curve is Hat. These are the standard properties of marginal and average cost curves. When the cost of a marginal unit exceeds the cost of an average unit then the average cost increases with the addition of the 7 As (In- lime imii sin inks n t.ilnr it> lln- In nut in.iliuily n. ihe loi intil.i (lll.l.H) appi n.u lies / i = Y i S и ilT >l i. м-pci inil vii lil plus ii times lite stupe >! tlx- vielil i uric at maturity и. 10.1. Hasic Concepts marginal unit, so the average cost rises when the marginal cost is above the average cost. Conversely, the average cost falls when the marginal cost is below the average cost. J 10.1.2 Coupon Bonds As we have already emphasized, a coupon bond can be viewed as a package of discount bonds, one with face value equal to the coupon for each date at which a coupon is paid, and one with the same face value and maturity as the coupon bond itself. Figure 10.3 gives a time line to illustrate the time pattern of payments on a coupon bond. The price of a coupon bond depends not only on its maturity n and the dale t, but also on its coupon rate. To keep notation as simple as possible, we define a period as the time interval between coupon payments and С as the coupon rate per period. In the case of US Treasury bonds a period is six months, and С is one half the conventionally quoted annual couponlrate. We write the price of a coupon bond as Pcnt to show its dependence on the coupon rate. The per-period yield to maturity on a coupon bond, Ycnl, is defined as that discount rate which equates the present value of the bonds payments to its price, so we have P = (Г + о + --+о- (10Л-9) In the case of US Treasury bonds, where a period is six months, Ycnt is the six-month yield and the annual yield is conventionally quoted as twice Ytnl. Equation (10.1.9) cannot be inverted to get an analytical solution for Ycnt- Instead it must be solved numerically, but the procedure is straightforward since all future payments are positive so there is a unique positive real solution for Ycn,.* Unlike the yield to maturity on a discount bond, the yield to maturity on a coupon bond does not necessarily equal the per-period return if the bond is held to maturity. That return is not even defined until one specifies the reinvestment strategy for coupons received prior to maturity. The yield to maturity equals the per-period return on the coupon bond held to maturity only if coupons are reinvested at a rate equal tothe yield to maturity. The implicit yield formula (10.1.9) simplifies in two important special cases. First, when Prnt = 1, the bond is said to be selling at par. In this case the yield just equals the coupon rate: Ycnl = C. Second, when maturity n Wit Ii negative future payments, tliere ran be multiple positive real solutions to (10.1.9). In the analysis of investment projects, the discount rate thai equates the present value of a project to its cost is known as the internal mlr of rrlum. When projects have some negative cash Hows in the future, there can be multiple solutions for the internal rate of return.  is infinite, ihe bond is called a consul or fmpHuity. In this ease the yield just equals die ratio of the bond price lo the coupon rate; )rtV), = C/lr00l. Duration and Immunization For discount bonds, maturity measures the length of time that a bondholder has invested money. But for coupon bonds, maturity is an imperfect measure of this length of lime because much of a coupon bonds value comes from payments that are made before maturity. Macaidays duration, due to Macaulay (1938), is intended lo be a better measure; like maturity, its units are time periods. To understand Macaulays duration, think of a coupon bond as a package of discount bonds. Macaidays duration is a weighted average of the maturities of the underlying discount bonds, where the weight on each maturity is the present value of the corresponding discount bond calculated using the coupon bonds yield as the discount rale:1 -.111- , I i , (1 + ) ) (It У. У (H T.,.,r Il nl - ----- i in ,} nit rv i (i + ); i (i + >, ,r (10.1.10) The maturity of the first component discount bond is one period and this receives a weight of C/( 1 + Ytnl), the present value of this bond when Yr, is the discount rate; the maturity of the second discount bond is two and this receives a weight of C/(l + Ytn,)1; and so on until the last discount bond of maturity n gels a weight of (1 + (.)/(1 + Y, ,) . To convert ibis into an average, wc divide by the sum of the weights C/(I -f >> ,) -f C/(l + Yt ,f + + (14- C)/(l + У ) , which from (10.1.9) is just the bond price / . These calculations are illustrated graphically in Figure 10.3. When С = 0, the bond is a discount bond and Macaidays duration equals maturity. When С > 0, Macaidays duration is less than maturity and it declines with the coupon rate. For a given coupon rate, duration declines with the bond yield because a higher yield reduces the weight on more distant payments in the average (10.1.10). The duration formula simplifies when a coupon bond is selling at par or has an infinite maturity. Л par bond has price lrn, = 1 and yield Y, , = C, so duration becomes Dc , = (1 - (1 + K ) )/(l - (1 + Yt ,)~l). A consol bond with infinite maturity has yield FrOOI = C/l[<xl so duration becomes Of0oi = С + F,<x>i)/ Froo(. Numerical examples that illustrate these properties are given in fable 10.1. The table shows Macaidays duration (and modified duration, defined in (10.1.12) below, in parentheses) for bonds with yields and coupon Macaulay also suggcsl-s that one could use yields on discount bonds rather than ibc yield on the coupon bond lo calculate the present value of each coupon payment. However this approach teitiii4s lhat one measure a complete /cro-coupou term sunt lure. / О. Fixed! тате Set unties Table 10.1. AUutiutass anil mmiijied duration Jor seterted bonds Maturity (years)

Couponrate Yield Coupon rate 10% Meld

I In- table .< ,., ,s Macaulays duration and. in parentheses, modified duration lor bonds with selected yields . I maturities. Duration, yield, ami maturity are staled in ;.....ual units b , tlie tutdct lying tabulations assume ibai bond payments are made at six-tuonih intervals rates <>l0%, D%, and 10%, and maturities ranging from one year lo infinity. Duration is given in years but is calculated using six-month periods as would be appropriate lor I IS Treasury bonds. II wc take Ihe derivative 1(10.1.0) wj respect lo } , or equivalently with respect lo (1 4 ) ), we find thai Macaulays duration has another very 10.1. Basic Concepts important property. It is the negative of the elasticity of a coupon bonds price with respect to its gross yield (1 4- Kf ,):10 Dnl =--+ (10in) d(\ + Ya ) l>(ut In industry applications, Macaulays duration is often divided by the gross yield (1 + Yc i) to get what is called modified duration: D,M dP 1 (10.1.12) (1 + Ynu) dYcnl Pcnt Modified duration measures the proportional sensitivity of a bonds price to a small absolute change in its yield. Thus if modified duration is 1(, an increase in the yield of 1 basis point (say from 3.00% to 3.01%) will cause a 10 basis point or 0.10% drop in the bond price. Macaulays duration and modified duration are sometimes used to answer the following question: What single coupon bond best approximates the return on a zero-coupon bond with a given maturity? This question is of practical interest because many financial intermediaries have long-term zero-coupon liabilities, such as pension obligations, and they may wish to match or immunize these liabilities with coupon-bearing Treasury bonds.12 Although today stripped zero-coupon Treasury bonds are available, they may he unattractive because of tax clientele and liquidity effects, so the immunization problem remains relevant. If there is a parallel shift in the yield curve so that bond yields of all maturities move by the same amount, (hen a change in the zero-coupon yield is accompanied by an equal change in the coupon bond yield. In this case equation (10.1.11) shows that a coupon bond whose Macaulay duration equals the maturity of the zero-coupori liability (equivalently, a coupon bond whose modified duradon equals the modified duration of the zero-coupon liability) has, to a first-order approximation, the same return as the zero-coupon liability. This bond-or any portfolio of bonds with the same duration-solves the immunizadon problem for small, parallel shifts in the term structure. Although this approach is attractively simple, there are several reasons why it must be used with caution. First, it assumes that yields of all maturities move by the same amount, in a parallel shift of the term structure. We Tlie elasticity of a variable В with respect to a variable Л is defined to be the derivative of Л wiili respect to A, times A/0: ((l(i/(fA)(A/fl). Equivalently, il is the derivative of log(B) with respect to log(A). 1 Note that if duration is measured in six-month time units, then yields should be measured on a six-month basis. One can convert to an annual basis by halving duration and doubling yields. The numbers in Table 10.1 have been annualized in this way. -htiinuni/.aiion was originally defined by Reddington (1952) as the investment of the assets in such a wa that the existing business is immune to a general change in the rale of interest . Kaboz/i and Fabozzi (1005), Chapter 42, gives a comprehensive discussion. 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 [ 68 ] 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 |